Last year was historic on many fronts as it relates to the market and volatility. This includes downside volatility (markets declines), along with Fed action that investors have not experienced in decades. Prior to this, we experienced a strong market for almost the past 13 years and now many individuals are curious as to what prudent action to take after this increased choppiness.

BentOak Capital is a financial planning first firm, as we have strong convictions that the financial plan is the cornerstone of the relationship. Through the planning process we take a holistic view of our client’s situation (e.g., tax planning, insurance, estate, etc.). We view all these in conjunction with the investment accounts. While many advisors manage investment accounts for clients, there are often accounts outside of their management. These could be separate brokerage accounts, current 401k’s or a 401k from a previous employer, or perhaps an annuity. These outside accounts or assets (e.g., real estate, precious metals, mineral interests, etc.) are important to incorporate in a plan and investment process to have that comprehensive view of the overall asset allocation. This is crucial, because often many of these accounts or assets are not included when looking at one’s allocation and risk profile to determine an appropriate amount of diversification.

Diversification is a word that gets thrown around a lot in our industry but doesn’t always get the respect it deserves. Many folks might think they are well diversified simply because they own a lot of “stuff” – dozens of ticker symbols perhaps. In good times, diversification may even get ignored, and there is wisdom in the words of Warren Buffett when he said, “only when the tide goes out do you discover who’s been swimming naked.” This is why understanding – or working with an advisor that truly understands – what your portfolio is constructed of is critical. It’s in volatile times that a lack of diversification may come to light.

We should note that diversification doesn’t necessarily protect investors from broad-based market downturns like we are experiencing now, but it does help ensure that investors can avoid being the embarrassed and vulnerable swimmer that Mr. Buffett referenced. Below are two examples of common diversification missteps – 1) not knowing what you own and 2) being overconfident in a particular company or sector.

Diversification Example #1: Not knowing what you own

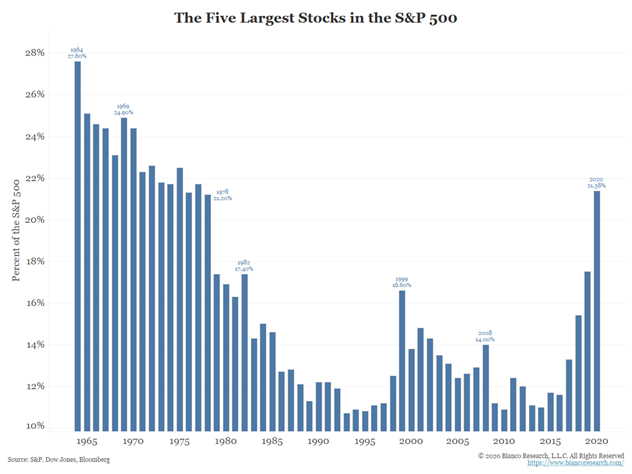

Our first example is somewhat of an often-overlooked issue: traditional indices, such as the S&P 500, may not provide enough diversification. Many individuals have exposure to an S&P 500 fund in some fashion, which is a great way to seek broad domestic large cap diversification. One item to note on the S&P 500 index is that it is market cap weighted. This means that as the market cap, or value of a company, grows then its weighting in the S&P 500 (or similar market cap weighted funds) does as well. That’s not necessarily a bad thing, but in recent years some companies have grown substantially. As of the end of 2021, approximately 24% of the S&P 500 holdings were Apple, Microsoft, Amazon, Alphabet (Google), and Tesla (see below). It is important to realize the weight these companies represent in an S&P 500 fund, and the respective account/portfolio. Also, if there is inflows into a particular sector or stock this may also be another contributing factor to its performance and market cap weighting in an index such as the S&P 500.

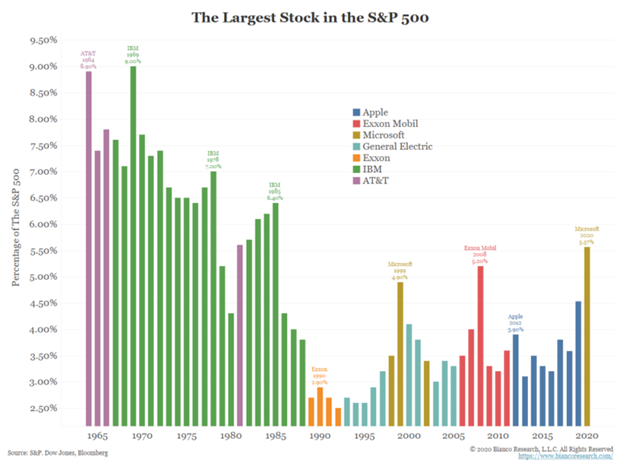

To take this a step further, if you were to drill into what company made up the largest position in the S&P 500 you might be surprised to find how large an individual stock might be. The chart below reflects this data and it is not a surprise in recent years to see specific companies being the largest, given what was seen in those respective sectors at that time (e.g. 2012-2019 the technology sector outperforming and Apple and Microsoft being the largest weighting.

In a case like this, you would want to make sure that there is not an overallocation to one of these positions in another account you have, or that there is not hidden overlap in other mutual funds you own. You can ensure strong diversification by not only owning a swath of large cap companies such as those the S&P 500 represents but by also owning additional asset classes such as mid and small cap US stocks, international stocks, real estate, and fixed income (bonds).

Diversification Example #2: being overconfident in a particular company or sector

Another common diversification issue is concentration in a single holding or sector. Often this stems from 401k plans that match employee contributions with company stock. The company match you receive is the most efficient growth you will have as you accumulate assets. With your employer matching, you are essentially doubling the amount you have contributed, which is something that is difficult to obtain elsewhere in investing – an immediate 100% return. While this is a nice retirement perk, there are also a few items to be aware of. Many companies make this match with company stock. Contributions in this form provide a great incentive to employees for the company to do well, but a concentrated stock position needs to be regularly reviewed and revisited. If your company stock does well and appreciates in addition to the contributions, it can become an even larger weighting – potentially driving the majority of your returns, both positive and negative. But it is important to remember that it is just as possible to receive flat or negative returns as it is to receive extremely positive returns.

To further illustrate the need for rebalancing a concentrated position, there have been a number of companies in the recent past that have gone through the bankruptcy process or some form of restructuring. Below is a table of some of the larger companies that have declared bankruptcy in the past 20 years. There are varying reasons behind each ranging from fraudulent activity (Enron, WorldCom), effects of the Great Recession/Financial Crisis (Lehman Brothers, Washington Mutual, General Motors), or a company that did not adapt to changing conditions (Eastman Kodak, Toys R Us Inc.). Many of these companies were established household names but provide an excellent example of having concentration risk in your portfolio. This concentration risk could be from an affinity bias, perhaps a position was inherited, or it could be the company you work for or worked in the past. Whatever the case, history has shown that mismanagement at the highest level of these companies can occur, and it can be devastating for individual investors.

| Selected US Companies Declaring Bankruptcy: 2000-Present | ||||

| Bethlehem Steel (2001) | General Growth Properties (2009) | Coldwater Creek (2014) | ||

| Enron (2001) | General Motors (2009) | Gymboree (2017) | ||

| WorldCom(2002) | Nortel Networks (2009) | Payless (2017) | ||

| Circuit City Stores (2008) | Borders Group (2011) | Toys R Us Inc. (2017) | ||

| Delta Air Lines (2008) | Patriot Coal (2012) | Sears (2018) | ||

| Lehman Brothers Holdings (2008) | Eastman Kodak (2012) | PG&E (2019) | ||

| Washington Mutual (2008) | Excel Maritime Carriers (2013) | |||

| Source: BankruptcyData.com | ||||

There are more recent examples of companies that grew substantially over the years, either organically or through acquisitions, but might have interests into too many areas that do not truly align with their core business. For a variety of these circumstances you will then see a company possibly divest portions of the business because of pressure from investors, the board, or financially these separate entities are more valuable/profitable as a standalone company versus the whole. Even in recent history, there have been numerous instances where this has occurred and had a direct impact on the value of a stock.

Company stock is just one example – sometimes people fall in love with a brand or become very loyal to a company, which can cause them to overconcentrate their portfolio in that particular stock. You may love the ease of online shopping with the same or next day delivery, have fond memories of drinking a specific soft drink with grandpa, or maybe a great aunt left you shares of an energy company they worked for, and you are sentimental to the holding. No matter the reason for an affinity to a certain stock, never forget that having an overconcentration in a single stock can carry substantial risk – regardless of how healthy you think the company is.

What about bonds?

Stocks might be the first asset class that comes to mind when thinking about diversification or managing risk, but fixed income and bonds are also critical. This is sometimes referred to as the “boring” asset class, and seldom gets the attention in the media like stocks, but it is also an especially important one to focus on. In a normal environment, we always review a client’s overall fixed income allocation. What we have seen in the past 5 months with fixed income is something that many investors today have not experienced during their investing career. It has been a sobering reminder of how diversification within specific assets classes is helpful in working to manage the various risks out there, especially interest rate risk. In addition to the more common risks associated with fixed income, one that rears its head every few years is sovereign risk in parts of the world that are not as stable as some developed countries. A recent example of this is something that we are seeing currently in Ukraine, where our thoughts and prayers go out to the Ukrainian people and all effected by their aggressive neighbor. The conflict there is also obviously affecting their country, economy, and businesses. In 2014 when Russia “annexed” Crimea, it had a swift impact on their economy and the underlying bonds issued from Ukraine. Bond prices declined sharply in the aftermath and had an impact on “global” bond funds or international bonds funds that had exposure to these effected areas. We are again seeing this pressure on fixed income prices from that region. This is another example of knowing what investments are in your portfolio. Your advisor needs to be familiar with not only the high-level investments but also the underlying investments within those and what potential risks could be on the horizon.

Conclusion

Last year we saw a tremendous amount of volatility across both the equity and fixed income markets. With this, we also saw a number of sectors and companies that had been strong performers in recent years give back some of those recent gains. If you have an outside account that you have not looked at recently, now would be a great time to incorporate it in a comprehensive review. The market movement has provided an opportunity to rebalance your portfolio to its respective diversified allocation. If you have not recently reviewed your investment portfolio in this fashion, or do not have a comprehensive financial plan, contact us to coordinate an initial call with one of our advisors. Studies have shown that individuals with a plan in place feel more prepared and optimistic than those without one. Let us help you identify your needs, goals, and objectives to create a plan, review it on an ongoing basis, and work to provide confidence for the future ahead.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.