A bear market is officially here thanks largely to stubbornly high inflation. For many of us, it has probably felt like a bear market for a while now, but the S&P 500 Index didn’t close more than 20% below its January 3 record high until Monday. Tech stocks are down a lot more—the Nasdaq Composite is more than 32% below its November 2021 record high.

It’s hard to find a silver lining in inflation over 8%, but here’s the good news. Goods inflation came down quite a bit, which is likely to continue. Also keep in mind that the Federal Reserve’s (Fed) preferred inflation measure, the core personal consumption expenditure index (PCE) is just under 5% (the next core PCE report is due out on June 30). The PCE inflation reading factors in product substitutions, making it a better reflection of how consumers are actually coping in this tough environment.

For those worried the Fed may be overly aggressive in its fight against inflation, consider the market has done a lot of work already. Home price appreciation has slowed on higher mortgage rates. Lower stock values will likely slow spending. Margin balances have fallen. Wage increases have leveled off as layoff announcements and pulled job openings have started to hit the newswires. The cost of credit has increased based on investment-grade and high-yield corporate bond spreads. Financial conditions are already tightening early in the Fed’s campaign. This is all actually good news, since these factors suggest the Fed may pause its rate hiking campaign in the fall.

Keep in mind a good part of the inflation problem is on the supply side (COVID-19, supply chain disruptions, Russian oil sanctions), so there’s only so much the Fed can do by curbing demand. While some of these supply issues may take many months to resolve, we believe they will be resolved before long. While oil prices are a wildcard, we are confident that a sizable piece of the inflation problem will get better in the months ahead and that patient investors will be rewarded.

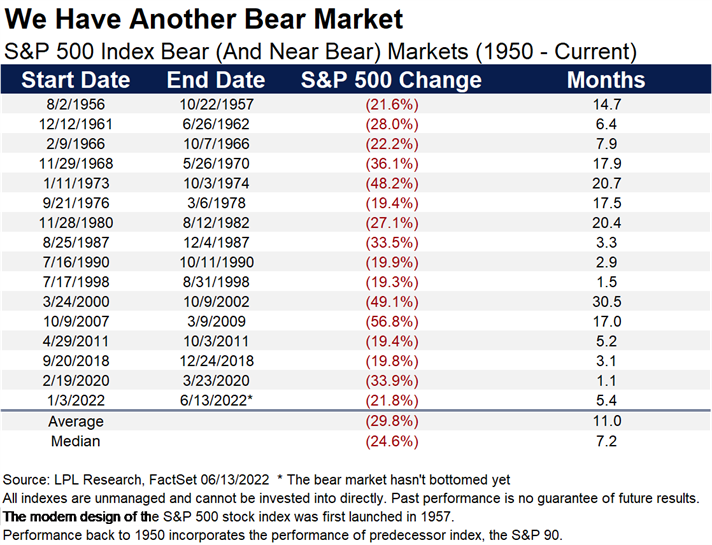

So now that the bear market is here, what should investors expect? Stocks are near their average decline in a bear market without a recession at about 24%, potentially introducing an attractive risk-reward trade-off for stock buyers here. The job market and consumer balance sheets simply look too strong for a major recession to come soon. Though no one knows what the future holds, Monday’s trading session also got us closer to the type of capitulation and indiscriminate selling that has marked prior major lows. The VIX measure of implied stock market volatility rose above 35 on Monday, close to the 40 level that has accompanied other major lows and suggesting an eventual market bottom may not be far off.

Here’s another encouraging statistic to help investors stay the course. After the S&P 500 enters a bear market, the median 12-month gain has been 24% with advances in seven of the past 10 instances back to 1957 (only 1973 and 2008 saw big declines). Even better, the average historical 12-month gain off a midterm election year low is over 30%.

In closing, don’t forget that lower stock prices can lead to attractive valuations, improving prospects for future returns. It’s tempting to sell, but history tells us that after big declines it can be the wrong move.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

All data is provided as of June 14, 2022.

All index data from FactSet.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Personal consumption expenditures (PCE) is a measure of price changes in consumer goods and services released monthly by the Bureau of Economic Analysis (BEA). Personal consumption expenditures consist of the actual and imputed expenditures of households; the measure includes data pertaining to durables, nondurables, and services. It is essentially a measure of goods and services targeted toward individuals and consumed by individuals.

The VIX is a measure of the volatility implied in the prices of options contracts for the S&P 500. It is a market-based estimate of future volatility. When sentiment reaches one extreme or the other, the market typically reverses course. While this is not necessarily predictive it does measure the current degree of fear present in the stock market.

This Research material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.