Inflation and interest rates have been the media’s main headliners for most of 2022, and with good reason – this is the highest inflation has been in more than three decades and interest rates have reached levels last seen well over a decade ago. Though this term is likely growing old for many of us, we are in unprecedented times, and the key to navigating times of uncertainty is relying on fact versus fiction. As we have mentioned in previous blog posts, there is a lot of noise right now with no shortage of opinions. Understanding inflation, the different measures of inflation, and how interest rates can affect inflation is a good start to sifting through the noise.

What is Inflation

Inflation is defined as a general increase in prices and fall in the purchasing power of money. For most investors, the basic concept may seem straightforward. However, a “general increase in prices” begs one to ask – prices of what, exactly? There are many ways to gauge inflation, but there are three main measures of inflation that we believe the Federal reserve is most closely watching as they carry out their interest rate hiking campaign to tame increasing prices.

Consumer Price Index (CPI)1

- The Consumer Price Index measures the overall change in consumer prices based on a representative basket of goods and services over time.

- The CPI is the most widely used measure of inflation, closely followed by policymakers, financial markets, businesses, and consumers.

- Housing rents are used to estimate the change in shelter costs including owner-occupied housing that account for nearly a third of the CPI.

Personal Consumption Expenditures (PCE)2

- PCEs include how much is spent on durable and non-durable goods, as well as services.

- The PCE Price Index is the method used by the Federal Reserve to measure inflation.

- The PCEPI is based on prices from all households, corporations, and governments, along with gross domestic product (GDP).

Producer Price Index (PPI)3

- The Producer Price Index measures change in the prices paid to U.S. producers of goods and services.

- The PPI is a measure of wholesale inflation, while the Consumer Price Index measures the prices paid by consumers.

- The indexes calculate price changes in private contracts based on suppliers’ input prices

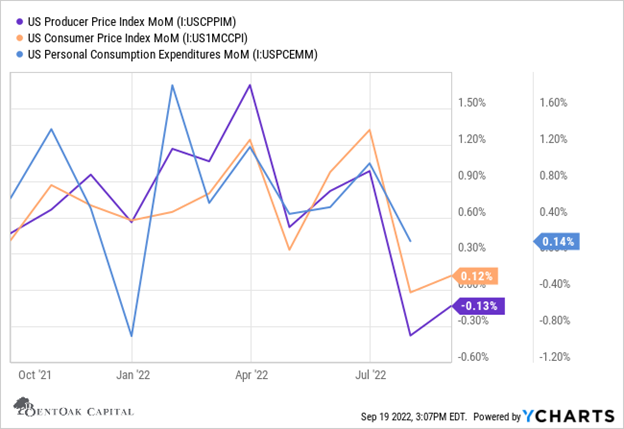

To summarize the three, CPI measures inflation by consumer prices, PCE measures inflation by how consumers actually spend, and PPI measures the wholesale (or input) prices that producers pay before they are marked up to be sold to consumers. It’s important to note that PCE is the Federal Reserve’s preferred measure of inflation, so when the Fed discusses inflation targets of 2%, this is the indicator they are referencing. PCE could be viewed as the more practical measure since it reflects the decisions that consumers make in light of inflation. For example, many households may choose a less costly alternative when they are feeling squeezed at the cash register (i.e. substituting pork for beef, canned vegetables for fresh produce, etc.). Because PCE accounts for the changes and decisions consumers make, it could be viewed as a more direct gauge of the economic impact of inflation to consumers.

Since PPI serves as an inflation measure for the producers of goods, it can be viewed as a leading indicator for consumer inflation. Producers will price goods based on the amount they had to pay for the materials to create the final product, which means there can be a lag time for price changes to reach consumers due to inventory effects and production time. We believe this lagging effect could be unfolding as we speak since PPI has contracted over the past couple of months as commodity prices & freight rates have deteriorated though there has not yet been a meaningful decline in either CPI or PCE. So, while consumer inflation continues to run hot, we do expect to see the rate of change slow over the coming months if this trend with PPI continues.

Headline vs. Core Measures

An often-mischaracterized notion is that the federal government does not include food and energy prices in their inflation measures – this is partially true but taken out of context. There are two different ways that CPI, PCE, and PPI are reported: 1) headline and 2) core. Headline inflation measures inflation for all an economy’s commodities, goods, and services. Core inflation measures the same data points but strips out more volatile food and fuel prices. Food and energy are removed from the core measure not because the Fed thinks they don’t matter – it’s because those prices can be very volatile on a month-to-month basis, which makes it more difficult to enact long-term monetary policy decisions with price trends changing rapidly.

The Current Inflation Dilemma

In addition to core inflation being a more stable measure with less short-term volatility, current food and energy costs are more supply oriented than they are demand oriented, and the Fed can only directly affect demand with monetary policy. The Federal Reserve can influence inflation through contractionary monetary policy (raising rates) and open market operations (buying / selling of government securities), both of which affect the money supply and consequently inflation. By raising interest rates, the Fed encourages banks and lenders to increase rates on riskier loans and move more of their money to the no-risk Federal Reserve, thereby reducing the money supply, which has the effect of reducing inflation.

Here is the current dilemma for the Federal Reserve: they can fight inflation by raising rates and restricting monetary policy, which will eventually help put a lid on certain consumer prices by dampening demand, but we do not really have a demand problem. Consumer prices are not increasing because consumer demand for all goods is on the rise. Yes, easy monetary policy and stimulus played a major role in creating higher than average inflation, and current wage inflation is correlated with consumer inflation. However, we believe lingering pandemic supply chain issues, continued lockdowns in China, weather, and geopolitics are several of the factors that have made it harder for the Fed to combat inflation.

In simple terms, the Fed might be able to raise interest rates to the point that people will think twice about paying a premium for real estate at a significantly higher borrowing cost. But, increasing interest rates will do little to end a drought or the Russian invasion of Ukraine (both of which have helped exacerbate supply-related inflation issues). We believe that many of these supply problems will need to naturally work themselves out over time.

Inflation Expectations are Key

Inflation expectations are simply the rate at which consumers and/or businesses expect prices to rise in the future. They matter because actual inflation depends, in part, on what consumers expect it to be. If consumers expect prices to continue to move higher, then they will likely change behaviors and inflation then becomes a self-fulfilling problem. As seen in this chart, market-implied inflation expectations are seemingly well anchored. After spiking earlier in the year, market-implied inflation expectations have fallen back to levels seen earlier in the last decade. Moreover, markets expect inflation to average 2.25% over the five-year period, five years from now (2027-2032), which is the Fed’s preferred way to measure long-term market-implied inflation expectations. So, by one measure at least, inflation expectations remain anchored.

While the Fed is potentially hamstrung in their ability to fully fight current inflationary pressures, they will likely have to stay committed to increasing interest rates to make sure consumers and businesses don’t expect higher prices to continue. Inflation expectations became unanchored in the 1970s and it took three years and two recessions to bring inflation expectations back to more normal levels. That is not something the Fed would like to repeat, which is probably why they have raised rates so strongly and swiftly to help temper long-term inflation expectations. Markets are currently anticipating that rates will continue to increase into March of 2023.

While the Fed is potentially hamstrung in their ability to fully fight current inflationary pressures, they will likely have to stay committed to increasing interest rates to make sure consumers and businesses don’t expect higher prices to continue. Inflation expectations became unanchored in the 1970s and it took three years and two recessions to bring inflation expectations back to more normal levels. That is not something the Fed would like to repeat, which is probably why they have raised rates so strongly and swiftly to help temper long-term inflation expectations. Markets are currently anticipating that rates will continue to increase into March of 2023.

What it Could Mean for Markets

It’s no secret that stock market returns have historically been stunted when inflation is at decade highs. However, something that is often overlooked is the concept of rising and falling inflation. When looking at the chart below, we have most likely been in a period similar to the one on the far left. Inflation has been high and increasing, leading to negative returns in global stock markets. We believe we could be in a period of time where inflation is still moderately high yet decreasing slowly, which is in line with data we have seen over the past couple of months. If this is the case, similar periods in the past have seen stock markets with solid gains – this is the second scenario from the left on the below chart.

So, while the pace of inflation may not be falling fast enough from the early summer highs for the Fed to upend their rate hike cycle just yet, we are seeing early signs of disinflation (meaning, when prices are still rising, but at a much slower pace than they had been) with PPI numbers. And if history is any guide, PCE and CPI could follow, which has traditionally been good for markets.

Conclusion

The inflation issue we are all currently facing is multifaceted; it isn’t as easy as raising rates to restrict demand, but that is essentially the only tool the Fed has at its disposal. In other words, the Fed’s toolbox only contains a hammer, and unfortunately, when you are a hammer, everything looks like a nail. So, while the Fed continues to hammer on interest rates to keep inflation expectations in check, we are monitoring PPI, commodity prices, and other supply indicators for improvement. We do not believe market participants are expecting immediate bright, sunshiny days, but we do believe markets will respond positively to a break in the clouds with clearer skies on the horizon.

IMPORTANT DISCLOSURE INFORMATION: Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by BentOak Capital [“BentOak”]), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. BentOak is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for personalized investment advice from BentOak. Please remember that it remains your responsibility to advise BentOak, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request at www.bentoakcapital.com/disclosure. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement. Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your accounts; and, (3) a description of each comparative benchmark/index is available upon request. Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any designation, certification, or license should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if BentOak is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, BentOak did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of BentOak by any of its clients. ANY QUESTIONS: BentOak’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.