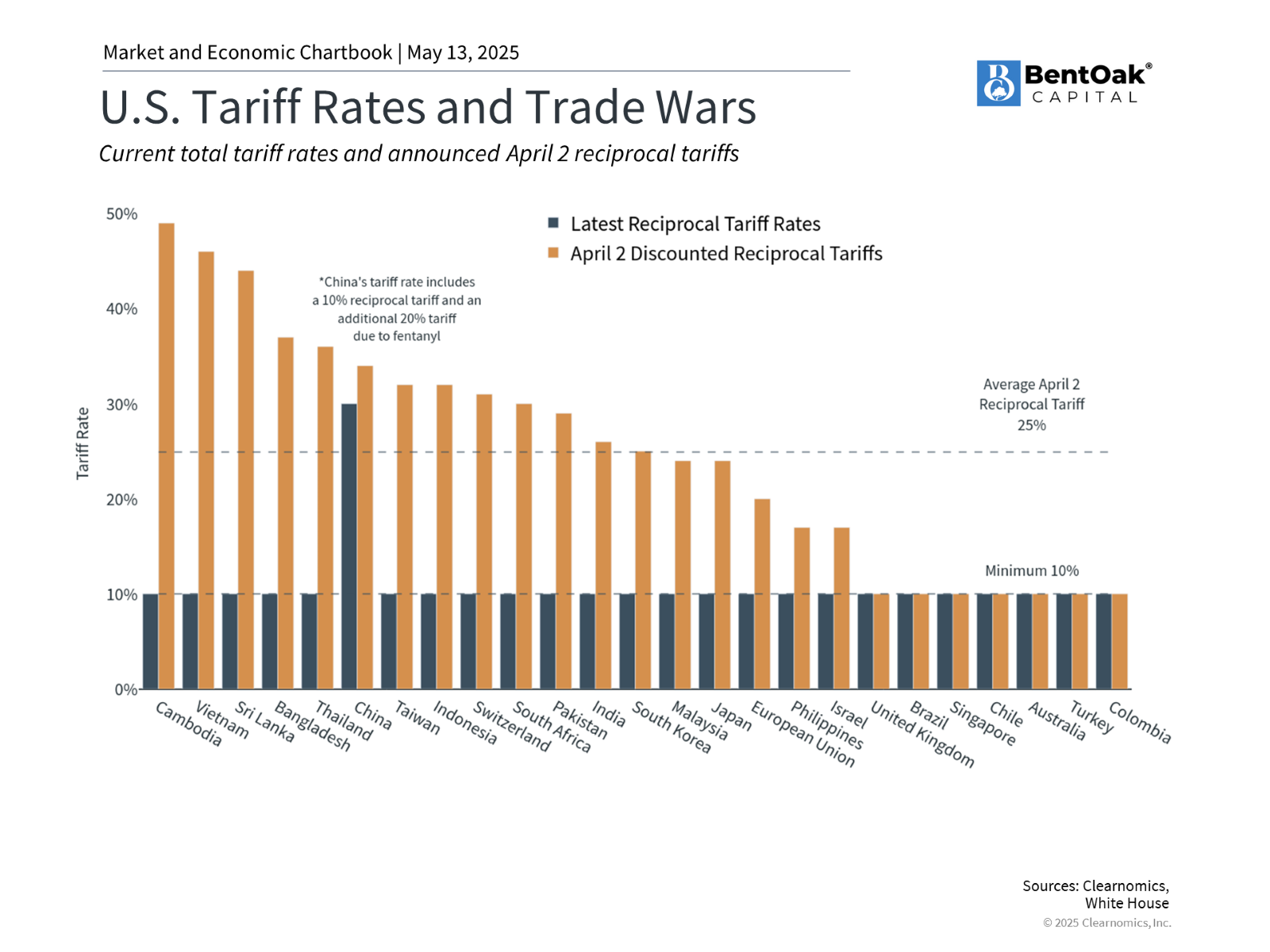

A significant breakthrough in U.S.-China trade relations has emerged over the weekend with a new agreement rolling back many of the tariffs that caused market turbulence beginning in April. The 90-day reprieve reduces U.S. tariff rates on Chinese imports from 145% to 30%, while China’s rates on American goods drop to 10%1. Combined with tariff suspensions involving other trading partners and a freshly announced trade agreement with the U.K., investors are increasingly confident that an extended trade conflict may be avoided. How should long-term investors interpret this evolving market narrative?

Financial markets respond most negatively to uncertainty and unexpected developments. This occurs because market participants often price in worst-case scenarios immediately before adjusting as additional information becomes available. While the unexpected magnitude of the April 2 tariffs triggered a sharp market decline, we’ve witnessed an equally rapid recovery in recent weeks.

Markets have nearly returned to their beginning-of-year levels and slightly exceeded their position prior to the April 2 tariff announcement. This pattern aligns with numerous historical examples where recoveries materialize once greater clarity emerges. Recent events further underscore the importance of maintaining a long-term investment perspective during periods of uncertainty.

The Recent Trade Arrangement Signals Potential for a Comprehensive Agreement

The newly established tariff agreement between the U.S. and China is seen by many experts as a potentially positive development, which could reduce a major source of market uncertainty. It establishes a 10% reciprocal U.S. tariff on Chinese goods while preserving the 20% tariff related to the fentanyl crisis implemented earlier this year. Although the situation continues to evolve, this agreement creates a foundation for a more comprehensive trade relationship between the world’s two largest economies and reduces tensions. Therefore, despite tariff rates remaining higher than historical levels, the probability of a worst-case scenario has diminished significantly.

Looking back, current events mirror the trade tensions experienced during the first Trump administration in 2018 and 2019. In both instances, the administration has employed tariffs as leverage to negotiate new trade agreements, explicitly aiming to reduce the U.S. trade deficit with major trading partners. Five years ago, this approach resulted in the “Phase One” trade agreement with China, the USMCA (United States-Mexico-Canada Agreement), and several other deals.

These trade policies encompass multiple interconnected objectives, including bolstering manufacturing employment, safeguarding intellectual property, managing immigration, and other priorities. The key distinction today is that the administration has advanced tariff threats more aggressively than many investors and economists had projected. Nevertheless, the recently announced U.S.-U.K. trade agreement suggests similar patterns may be emerging. This agreement establishes a baseline 10% tariff rate on British goods, with special provisions allowing importation of up to 100,000 vehicles at this rate and exemptions for steel and aluminum products.

Economic Indicators Remain Strong Despite Trade-Related Challenges

Certainly, comprehensive trade agreements with China and numerous other nations have yet to be finalized, and daily headlines may continue to drive market fluctuations, particularly if current tariff pauses expire. Markets have focused intensely on tariffs primarily due to their impact on inflation and economic growth. This was evident in first-quarter GDP data that revealed a slight economic contraction as businesses accumulated imported goods ahead of tariff implementation dates. Increased clarity will likely benefit both consumer and business confidence.

In this environment, what positive developments might unfold? First, numerous economic indicators continue to show strength. The most recent employment report revealed the economy added 177,000 positions in April, surpassing expectations of 138,000. The unemployment rate remained steady at 4.2%, continuing a period of stability that began last May. This robust labor market helps counterbalance concerns that tariffs and uncertainty might negatively affect consumer spending.

Simultaneously, inflation continues its gradual decline toward the Federal Reserve’s 2% target, with the latest Consumer Price Index measuring 2.4% year-over-year. This deceleration has been supported by declining oil prices, which recently reached four-year lows. Lower oil costs, partially influenced by tariff-related volatility, reduce expenses for consumers and can stimulate economic activity, all else being equal.

The recent U.S.-China agreement also diminishes pressure for immediate Federal Reserve policy adjustments. Market-based projections still anticipate Fed rate reductions this year, but expectations have moderated to only two or three cuts, potentially beginning in July or September. The Fed, which recently maintained rates between 4.25% and 4.5%, appears to be adopting a cautious approach rather than responding immediately to short-term trade, market, and economic developments.

Market Rebounds Frequently Occur When Least Anticipated

While numerous market risks persist, developments over recent weeks demonstrate how rapidly the prevailing narrative can shift. Markets inherently anticipate worst-case scenarios. During periods of negative headlines and market declines, envisioning a recovery becomes challenging. Therefore, while risk assessment remains prudent, it should not compromise long-term portfolio positioning.

The accompanying chart illustrates the behavior of market corrections since World War II. While the average correction involves a 14% decline, recovery typically occurs within approximately four months. Most importantly, markets often rebound when least expected, as we’ve witnessed following recent progress in trade negotiations. Investors who overreact to early signs of volatility may find themselves inappropriately positioned relative to their financial objectives.

The recent U.S.-China trade negotiations has contributed to reducing policy-related uncertainty and easing broader economic concerns. This development reflects a positive step toward more predictable global trade dynamics, which had previously weighed on investor sentiment and business confidence.

For long-term investors, this serves as a reminder of the value of maintaining a disciplined and long-term perspective, especially during periods of heightened market volatility. Reacting to short-term headlines or temporary fluctuations can often lead to suboptimal outcomes. Instead, staying focused on strategic goals and adhering to a well-constructed financial and portfolio plan remains essential to navigating market cycles effectively.

IMPORTANT DISCLOSURE INFORMATION: Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by BentOak Capital [“BentOak”]), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. BentOak is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for personalized investment advice from BentOak. Please remember that it remains your responsibility to advise BentOak, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request at www.bentoakcapital.com/disclosure. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement. Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your accounts; and, (3) a description of each comparative benchmark/index is available upon request. Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any designation, certification, or license should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if BentOak is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, BentOak did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of BentOak by any of its clients. ANY QUESTIONS: BentOak’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.