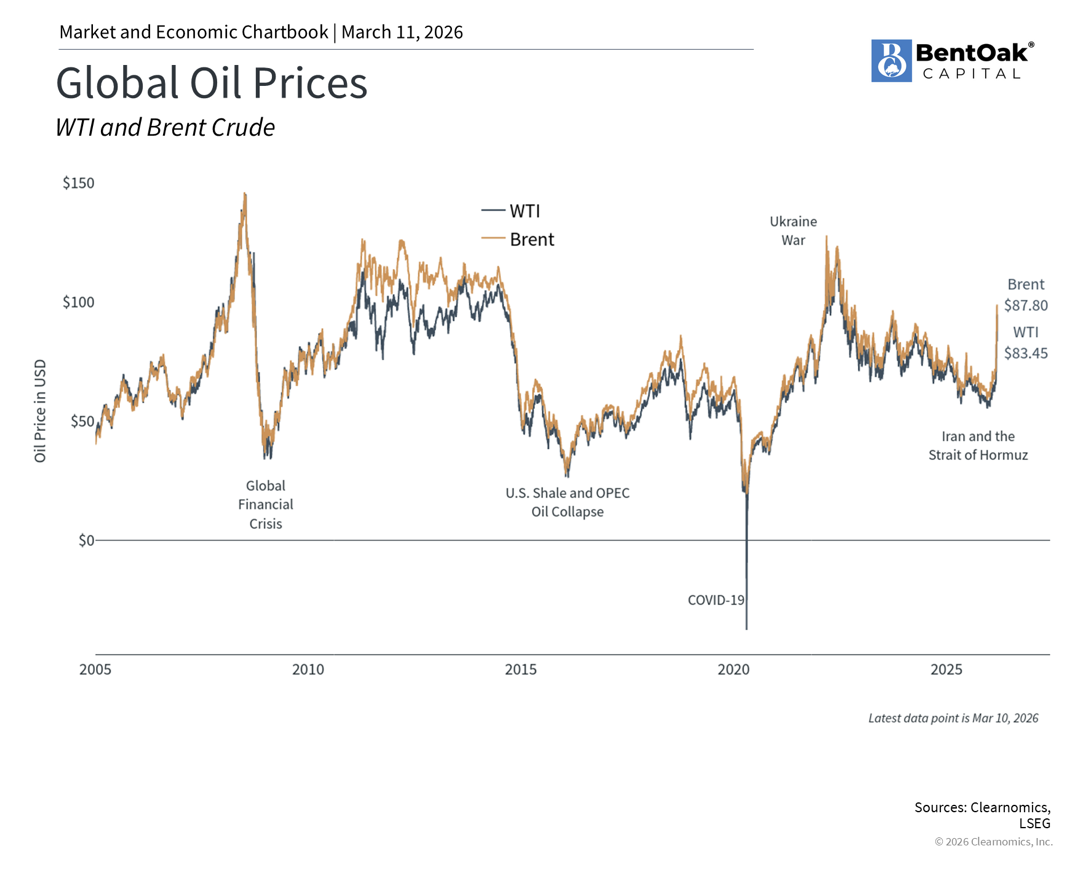

Escalating conflict in Iran and the effective closure of the Strait of Hormuz have sent oil prices sharply upward. Both Brent crude and WTI have surged from roughly $70 per barrel to approximately $100 in just a matter of days, nearing levels last observed in 2022 when Russia invaded Ukraine. This rapid rise has generated considerable uncertainty across global markets, with terms such as “global economic downturn” and “stagflation” appearing frequently in financial headlines.

Above all else, the safety of civilians and military personnel remains the foremost concern in any conflict. Even so, history generally suggests that maintaining a long-term perspective tends to be a prudent approach when navigating periods of heightened uncertainty from an investment standpoint. A quote often attributed to Mark Twain is “history doesn’t repeat itself, but it often rhymes.” This applies well to energy price shocks, which have materialized roughly every decade. Although each episode carries its own unique characteristics, a recognizable pattern emerges: oil prices surge in response to geopolitical tensions, markets experience volatility, and conditions eventually stabilize and recover.

The situation continues to evolve rapidly, and there are no certainties regarding when stability will return to the region or to financial markets. Recent events, including other Middle East conflicts, inflationary pressures, trade disputes, and developments in Venezuela earlier this year, all offer valuable context. With that in mind, what key considerations should investors keep in focus in the weeks ahead?

The drivers behind volatility in oil prices

For investors, energy prices represent the primary channel through which geopolitical events influence the broader economy and financial markets. The impact of any given conflict depends on how it alters the balance of supply and demand. Currently, elevated oil prices reflect disruptions to oil transportation, constraints on storage capacity, and production cuts by major oil producers across the Middle East. The potential length of the conflict is also a factor as Iran appoints a new supreme leader.

The focal point of the current oil price surge is the Strait of Hormuz, a narrow but critically important waterway linking the Persian Gulf to global markets. Approximately 20% of worldwide oil shipments and a significant portion of natural gas transit this chokepoint annually. While Iran cannot technically close the strait outright, attacks on tankers and mounting safety concerns have been sufficient to halt traffic. Leading shipping and logistics firms have restricted or suspended bookings through the area, leaving hundreds of oil tankers anchored inside the strait.

This disruption has produced a domino effect throughout the energy market. With tanker transportation through the Strait of Hormuz effectively stalled, major Middle Eastern oil producers have been compelled to store their output rather than export it. As storage facilities approach capacity, countries including Saudi Arabia, Iraq, Kuwait, Qatar, and the UAE have been forced to cut production. Unlike conventional OPEC production reductions aimed at supporting prices, these measures are involuntary and driven by necessity. This sequence of events explains why oil prices have risen so dramatically in such a compressed timeframe.

It is widely understood that when oil prices climb above $100, economic activity can begin to slow, putting pressure on household budgets and fueling inflation. Even so, it is important to place these moves in proper historical context. Although oil prices have remained relatively subdued over recent years, they have experienced significant swings over time. When Russia invaded Ukraine in early 2022, Brent crude surged to nearly $128 per barrel, pushing average gasoline prices in the U.S. above $5 per gallon. Prior to that, the mid-2000s saw oil reach record highs amid rapid global economic growth in the lead-up to the 2008 financial crisis. In each instance, prices ultimately stabilized as supply and demand rebalanced.

The impact of elevated oil prices on consumers and businesses

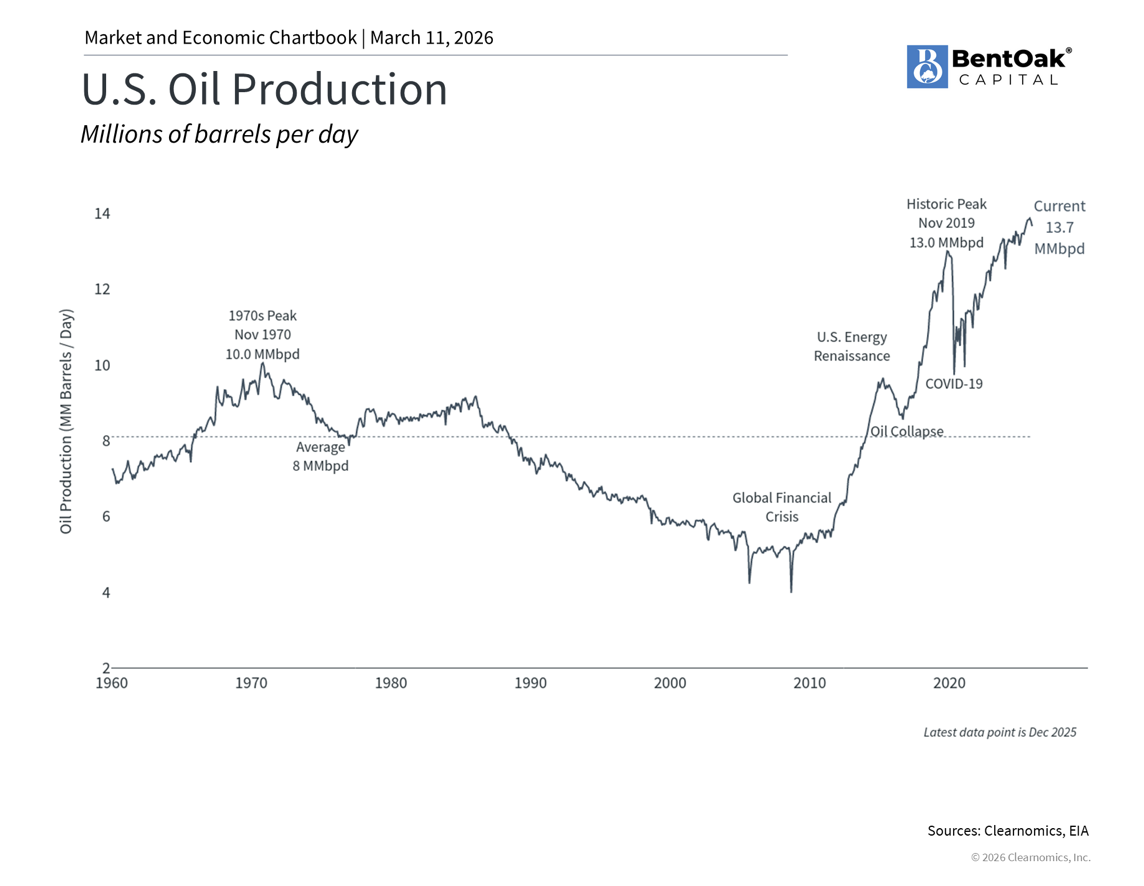

The U.S. is better positioned today than during prior oil crises, largely due to the shale revolution. As the world’s largest producer of both oil and natural gas, the U.S. enjoys a degree of energy independence that was absent during earlier historical oil shocks. Although oil remains a globally priced commodity and the U.S. still imports certain grades of crude, this self-sufficiency provides greater insulation for the domestic economy relative to those in Asia and Europe. The U.S. is also considered a “swing producer,” meaning it has the capacity to increase output when prices are elevated.

That said, higher oil prices still permeate every aspect of economic activity. For consumers, the most direct and visible effect is felt at the gas pump, where rising fuel costs cut directly into household budgets. At present, gasoline prices have climbed back toward $3.50 per gallon nationally and could move higher.2 While elevated, this remains meaningfully below the $5 per gallon level experienced four years ago.

Beyond the pump, there are numerous indirect effects on consumer prices more broadly. Higher energy costs increase the expense of transporting goods, manufacturing products, and operating businesses. In this respect, rising oil prices act as an effective burden on the economy by increasing the cost of virtually all goods and services and reducing disposable incomes.

Economists often describe this dynamic as “cost-push inflation.” When oil prices rise sharply, businesses face higher production costs that are ultimately passed along to consumers. This is distinct from demand-driven inflation, where prices increase because consumers are spending more freely, such as following the issuance of government stimulus payments.

This distinction is meaningful, because supply shocks are generally viewed by economists and market participants as “transitory”, meaning their effects are expected to diminish over time. This can occur either because geopolitical conditions improve and oil prices recede, or because the economy gradually adapts to a higher-price environment. While sudden energy price spikes are undeniably challenging, historical experience suggests they do not inflict permanent damage on the broader economy.

Financial markets have historically navigated oil price shocks

Despite these historical lessons, financial markets can and do react to oil price shocks in the near term. The S&P 500 is only down a couple of percentage points year-to-date, yet many headlines are drawing attention to declines such as South Korea’s KOSPI index and Japan’s Nikkei index declining since the end of February. What often goes unmentioned is there respective performance over the past year. Markets rarely advance in a straight line, and maintaining this broader perspective is essential.

At the same time, energy companies stand to benefit from higher prices. The energy sector has gained approximately 25% year-to-date, leading the broader market. Similarly, the commodities asset class has risen over 20% this year, supported by gains in both energy and precious metals. This is not an argument for concentrating portfolios in energy, but rather a reminder of the value that holding a variety of asset classes and sectors can provide.

Recent developments also introduce uncertainty around the Federal Reserve’s next steps. Should inflation accelerate due to higher oil prices, the Fed may need to maintain rates at a higher level than currently anticipated. At present, market-based expectations point to at least one rate cut this year in September, with the possibility of a second before year-end. However, if the supply disruption proves temporary, or if it persists for several months, its influence on monetary policy may ultimately be limited, consistent with historical precedent.

Of course, this does not preclude continued day-to-day market fluctuations. Rather, it reinforces the importance of well-constructed asset allocations and financial plans that are specifically designed to navigate these types of risks. Making significant portfolio changes in response to near-term headlines frequently proves counterproductive. Long-term investment success is more reliably achieved by maintaining diversified portfolios and staying committed to broader financial objectives.

Despite the recent conflict in Iran pushing oil above $100 and contributing to market volatility, history shows that financial markets and the broader economy have consistently adapted to similar supply side disruptions. In this environment, investors are best served by maintaining perspective, staying diversified, and keeping their focus on long term goals rather than reacting to day to day geopolitical developments or headlines.

1 https://www.eia.gov/todayinenergy/detail.php?id=65504

2 https://www.nytimes.com/2026/03/09/business/gasoline-prices-iran.html

IMPORTANT DISCLOSURE INFORMATION: Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by BentOak Capital [“BentOak”]), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. BentOak is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for personalized investment advice from BentOak. Please remember that it remains your responsibility to advise BentOak, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request at www.bentoakcapital.com/disclosure. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement. Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your accounts; and, (3) a description of each comparative benchmark/index is available upon request. Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any designation, certification, or license should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if BentOak is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, BentOak did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of BentOak by any of its clients. ANY QUESTIONS: BentOak’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.